Even if the now eight-week-old Iran War ends soon, some economists and analysts say the damage it’s already done will keep the U.S. economy on a narrow footing.

And that includes a holding pattern for benchmark interest rates which influence short-term borrowing from consumer credit cards to business loans, and indirectly, mortgage rates.

But not all experts are seeing a long pause to Fed rate cuts despite inflation, war and labor-market concerns.

Economists at BNP Paribas said in a note that “Our base case is for the Fed to remain on hold into 2027. That said, we see a growing tail risk that policymakers could consider hiking as soon as June if the Strait of Hormuz stays closed and U.S. labor data remains resilient,” reported The Business Times.

Meanwhile Eric Diton, president & managing director at The Wealth Alliance, told TheStreet that while the Fed remains committed to bringing inflation back to its 2% goal, it “must balance this with a labor market where the majority (80%) of jobs added in the past three years have been disproportionate from education and healthcare.”

Diton cited recent Blackrock research.

“However, sectors that employ a large share of white-collar and tech-adjacent workers have seen slower growth, opening the door to a potential rate cut later this year if the unemployment rate were to rise,’’ Diton said.

April FOMC meeting expected to hold rates steady

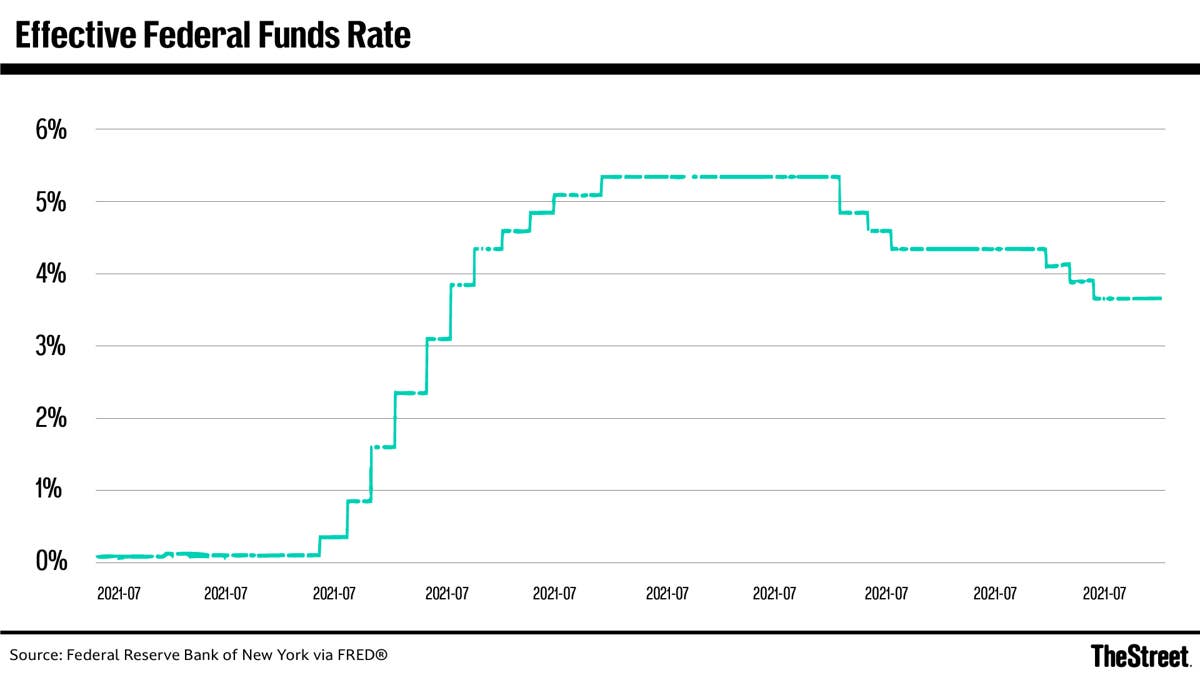

Traders at the CME Group FedWatch Tool are pricing in the next time the Federal Open Market Committee will cut benchmark interest rates as late 2027, almost four quarters later than what was expected at the beginning of this year.

More Federal Reserve:

- Fidelity delivers sobering interest-rate message amid Fed pause

There’s a 100% probability the FOMC will hold rates steady at its April 29 meeting, according to the FedWatch Tool.

The FOMC voted 11-1 March 18 to hold the benchmark Federal Funds Rate at 3.50% to 3.75%.

It was the FOMC’s second pause after cutting rates by 75 basis points during its last three meetings of 2025 due to a weakening labor market.

Fed’s dual mandate requires a balance of jobs, prices

The Fed’s dual congressional mandate is to ensure the U.S. economy is in balance with maximum employment and stable prices.

- Lower interest rates support hiring but can fuel inflation. This risks fueling further inflation, potentially leading to an inflationary spiral.

- Higher rates cool prices but can weaken the job market. This increases the cost of borrowing and further stifles economic activity.

Stagflation concerns rise with latest inflation, jobs and GDP rates

Billionaire investor Ray Dalio, the founder of Bridgewater Associates, told CNBC this week that the U.S. economy has devolved into stagflation, and the “wait-and-see approach” of the Fed is appropriate at least for the next several meetings to protect the economy from sliding into further risk.

Stagflation is a rare and challenging economic phenomenon characterized by the simultaneous occurrence of stagnant economic growth, high inflation and high unemployment.

Related: Incoming Fed Chair Warsh’s rate cut path is on a collision course with White House

- Headline PCE, the Fed’s preferred inflation gauge, rose to 2.85% in February. It’s the fifth straight year inflation has been higher than the Fed’s own 2% target.

- The March unemployment rate dropped to 4.3% in March from 4.4% in February and nonfarm payrolls added 178,000 jobs to significantly beat market expectations.

- Real GDP growth for the fourth quarter of 2025 was 0.5%, a sharp deceleration from the 4.4% growth seen in Q3.

Fed faces challenges to both sides of its mandate

Even before the outbreak of the eight-week Iran War, the Fed faced a dilemma from worrisome risks to both sides of its congressional mandate: unemployment rates and sticky inflation from tariffs.

Several Wall Street firms say inflation will now be closer to 3% this year than the Fed’s 2% target, eating into disposable incomes and keeping a lid on hiring.

That’s a shift from what was supposed to be a strong year in 2026 as the inflationary shock of President Donald Trump’s tariffs faded and stimulus from tax cuts kicked in.

Iran War’s impact on Fed’s inflation concerns

As I reported, Federal Reserve Governor Michael Barr said that while he was “hopeful” inflation falls this year, that ?might not happen with higher oil prices spiking gasoline and other consumer costs, mirroring increasing concerns from Main Street to Wall Street about the Fed’s interest-rate outlook due to recessionary and inflationary uncertainty.

“Moreover, the conflict in the Middle East raises additional risks. Higher oil prices tend to pass through pretty quickly to gasoline prices, and higher gasoline prices can be particularly painful for low- and moderate-income families,’’ Barr said in prepared remarks.

FOMC meeting expected to be Powell’s last as Fed Chair

The April FOMC meeting is presumed to beJerome Powell’s last as Fed Chair.

Former Fed Governor Kevin Warsh, President Donald Trump’s nominee to replace him, is expected to be approved by the Senate Banking Committee April 29.

The full GOP-led Senate is expected to approve Warsh by May 15 when Powell’s term as Fed Chair ends. Warsh has long been advocating a “regime change” at the central bank, including lower interest rates.

Trump has been demanding throughout his first and second administrations that Powell slash interest rates by 1% or less.

Cetera CIO Gene Goldman said in his latest weekly commentary that the “Fed remains effectively constrained by sticky inflation limits near-term cuts, while geopolitical volatility continues to cloud the growth outlook.’’

“Against that backdrop, even subtle shifts in tone from Powell could be read as setting the table for June under new leadership,” Goldman added.

Related: Markets reset Fed rate-cut bets as DOJ drops Powell probe

#Debates #Fed #rate #cuts #surprise